Many homeowners across the country feel a sudden sense of dread after signing a solar contract. You might have seen a smooth presentation about “free energy,” but now you face a massive debt. If you are looking to cancel Mosaic solar loan agreements, you are not alone.

Many people feel trapped. They deal with unfinished installs, pushy sales reps, or systems that don’t save money. This guide explains how to get out of Mosaic solar financing safely. At Solar Cancellation Companies, we will guide you about your rights, the risks of stopping payments, and the practical steps to regain your financial freedom.

How Mosaic Solar Financing Works

Mosaic’s Role in Solar Financing

Mosaic is not a solar installer. They are a financial technology company. They provide the money to pay your solar contractor. When you sign a contract, Mosaic pays the installer, and you pay Mosaic back over 10 to 25 years.

What Homeowners Usually Sign

You likely signed two separate documents. One is an installation agreement with the solar company. The other is a Mosaic loan agreement. These are legally linked but technically separate. If you are unsure which type of agreement you have, our Solar Contract Type guide explains the difference between a loan, lease, and PPA clearly.

When Solar Loan Funding Happens

Mosaic usually sends a “milestone payment” to the installer once the design is approved. The final payout happens after the panels are installed. Once the installer is paid in full, your Mosaic solar financing becomes much harder to reverse.

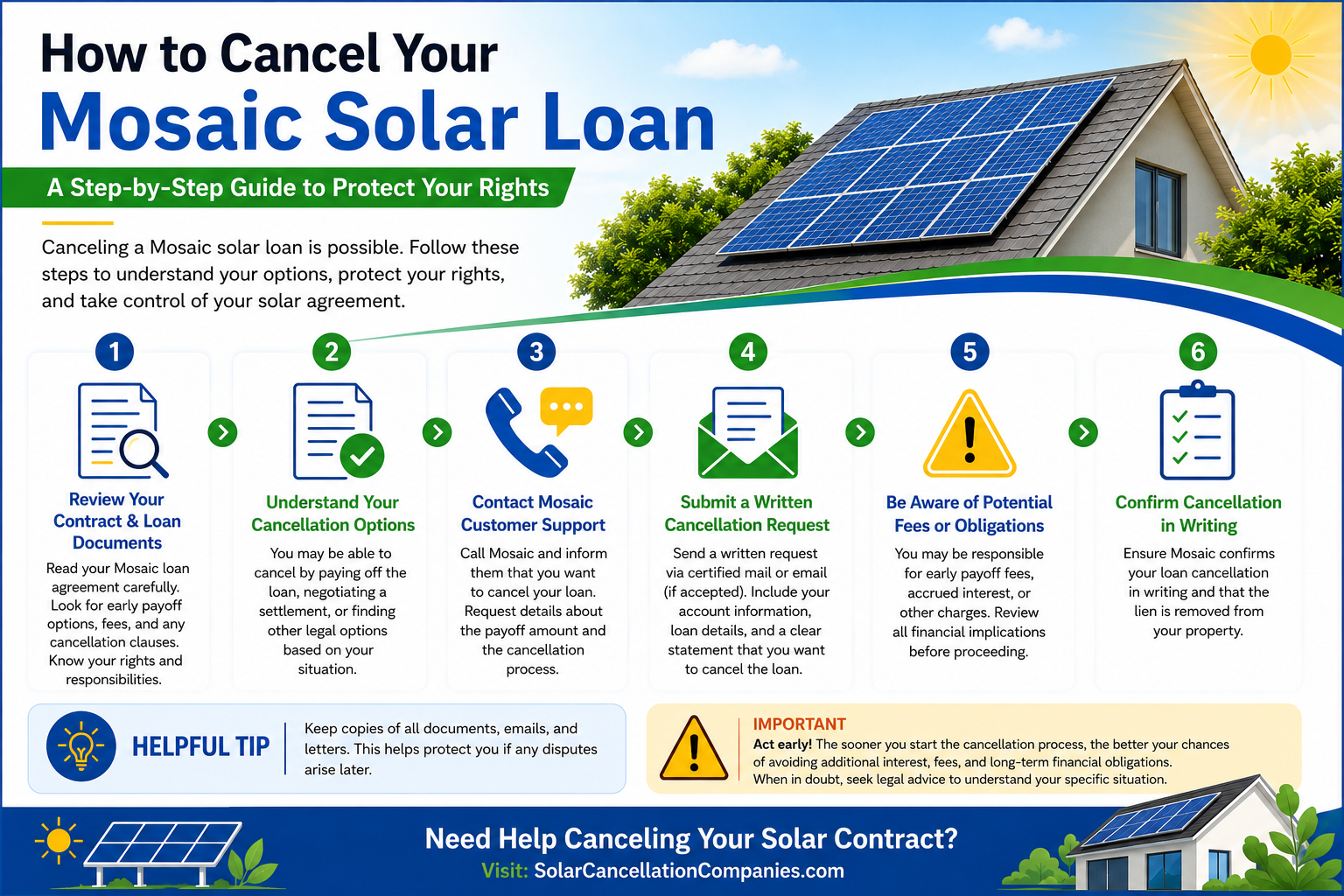

Can You Cancel a Mosaic Solar Loan?

When Cancellation May Be Possible

You can usually cancel without penalty within the “Right of Rescission” period. This is typically 3 business days. If the system is not yet installed, you have a better chance to cancel the solar contract financed by Mosaic.

Why Some Loans Remain Active After Cancellation

Even if you tell the installer to stop, the loan might stay open. If the installer does not “return” the funds to Mosaic, the bank still expects payment. This is a common source of Mosaic solar loan complaints.

Situations That Make Cancellation More Complicated

Cancellation becomes a major hurdle if:

- The panels are already bolted to your roof.

- The installer has already gone out of business.

- You have already signed a “Certificate of Completion.”

Why Homeowners Try to Get Out of Mosaic Solar Financing

Misleading Sales Promises

Many homeowners seek a Mosaic solar financing dispute because of “fake savings.” Sales reps often promise your electric bill will vanish. When the bill stays high and the loan payment arrives, reality sets in.

Installation and Performance Problems

If your system produces 50% less energy than promised, the loan feels like a scam. Many people want to cancel Mosaic solar loan agreements when the hardware fails and the installer won’t fix it.

Unexpected Financial Burdens

High interest rates and hidden fees can make the total cost double. This leads many to look for Mosaic solar financing legal options to escape the debt.

Installer Shutdowns and Bankruptcy Issues

If your installer goes bankrupt, you are often left with a broken system and a full loan. This is a primary reason for seeking a Mosaic loan agreement termination. Homeowners who financed through Mosaic but used installers like Freedom Forever have reported exactly this situation, where both companies are simultaneously in dispute.

Signs of Potential Solar Financing Misconduct

Red Flags During the Signing Process

Did the rep rush you through an iPad screen? Did they promise government “checks” that never came? These are signs of predatory lending.

Common Complaints in Mosaic Financing Disputes

Many homeowners report that their signatures were forged or that the loan terms changed after they signed. These are valid reasons to dispute a Mosaic financed solar contract.

How Dealer Fees Increase Total Solar Costs

Solar loans often have “dealer fees” hidden in the principal. This can add 20% to 30% to your loan before interest even starts. Understanding this is key to homeowner rights when canceling Mosaic solar financing.

What Happens if You Stop Paying a Mosaic Solar Loan?

Early Consequences of Missed Payments

If you stop paying, your credit score will drop quickly. Mosaic will report late payments to the bureaus. This can make it hard to get other loans.

Longer-Term Risks

Eventually, the account goes to collections. While solar lenders rarely foreclose on a home, they can place a lien on your property through a UCC filing.

Why Stopping Payments Does Not Automatically Cancel the Loan

Stopping payments is not a legal cancellation. It is the default. You must follow a formal Mosaic solar payment cancellation process to protect your credit.

How to Dispute a Mosaic Solar Loan

Common Reasons Homeowners File Disputes

- The system was never turned on.

- The installer committed fraud.

- The loan terms were misrepresented.

Documents That Can Help Support a Dispute

Keep every email, text, and flyer. You will need your original contract and any proof that the system is underperforming.

How to Escalate a Solar Financing Complaint

Contact Mosaic and the Installer

Start with a formal written letter. Send it via certified mail. Ask for a “Proof of Debt.”

File a CFPB Complaint

The Consumer Financial Protection Bureau (CFPB) oversees lenders like Mosaic. Filing a complaint here often gets a faster response.

Submit a State Attorney General Complaint

State AGs are cracking down on solar fraud. This is a great move for a Mosaic solar complaint Texas or a Mosaic contract dispute Florida. Check your state’s specific consumer laws on our Solar State Laws page.

Report Issues to Contractor Licensing Boards

If the installer messed up the roof, the licensing board can pressure them to cancel the deal.

Consult a Consumer Protection Attorney

If you are overwhelmed, search for a Mosaic solar financing lawyer in California or in your local area to review your contract for loopholes.

Legal and Financial Issues Homeowners Should Understand

Arbitration Clauses in Solar Financing Agreements

Most Mosaic contracts have an arbitration clause. This means you cannot sue them in a traditional court. You must go through a private process.

Can Homeowners Sue Over Solar Financing Problems?

Yes, but it is usually done through arbitration or small claims. If fraud is involved, an attorney can help you find legal options if a solar company used Mosaic financing unfairly.

Credit Score and Collection Concerns

Protecting your credit is vital. Sometimes, a “pay for delete” or a settlement is better than a long legal battle.

Mosaic Bankruptcy and Loan Servicing Concerns

What Mosaic’s Bankruptcy Means for Borrowers

Mosaic filed for Chapter 11 bankruptcy recently. For most homeowners, this doesn’t mean your debt disappears. It usually means your loan will be managed by a new “servicer.”

Loan Transfers and Servicing Changes

During a bankruptcy, your loan might be sold. You must ensure your payments are going to the right place so you don’t get hit with missed payments.

Problems Homeowners Report During Servicing Transfers

Lost paperwork and double billing are common during transfers. Keep meticulous records of every payment made.

Selling a Home With a Mosaic Solar Loan

Why Solar Financing Can Delay Home Sales

Buyers often refuse to take over a solar loan. They don’t want the extra debt. This can kill a home sale at the last minute.

Understanding UCC Filings

Mosaic places a UCC-1 filing on the solar equipment. This acts like a lien. You cannot clear the title of your home until this is addressed.

Options Homeowners Explore Before Selling

You may have to pay off the loan from your home sale proceeds or negotiate a loan settlement discussion to lower the payoff amount.

Common Real-World Solar Financing Scenarios

If the Installer Went Out of Business

This is a “Holder Rule” situation. Under federal law, you may be able to assert claims against the lender (Mosaic) that you had against the seller (the installer).

If the Solar System Never Worked Properly

You should not pay for a “brick” on your roof. Document the lack of production and file a formal Mosaic solar financing dispute.

If Installation Was Never Completed

If there are no panels, there should be no loan. If payments started, this is a major red flag.

If You Believe Your Signature Was Forged

Contact a lawyer immediately. Forgery is a crime and a clear path to cancel Mosaic solar loan obligations.

If Automatic Payments Continue After Cancellation

Contact your bank to stop the ACH transfer. Then, send a written notice to Mosaic that the authorization is revoked.

State Laws That May Affect Cancellation Rights

Solar laws vary. Some states like California have the “Solar Consumer Protection Guide” that installers must follow. If they didn’t, you might have a path to remove Mosaic financing after solar contract cancellation.

Alternatives to Canceling a Mosaic Solar Loan

Loan Settlement Discussions

If you can’t cancel, you might settle. You offer a lump sum (less than the total) to close the account forever.

Refinancing Options

You can sometimes roll the solar debt into a mortgage refinance with a lower interest rate.

Mediation and Negotiated Resolutions

A neutral third party can help you and Mosaic reach a middle ground, such as a lower monthly payment.

Installer Buyback or Removal Agreements

In rare cases, the installer can be forced to take the panels back and pay off your Mosaic loan.

Mistakes Homeowners Should Avoid

- Ignoring Loan Notices: This will only hurt your credit.

- Relying Only on Verbal Conversations: If it isn’t in writing, it didn’t happen.

- Throwing Away Key Documents: Your contract is your best weapon.

- Delaying Complaint Escalation: The longer you wait, the harder it is to prove fraud.

Frequently Asked Questions

How can I cancel my Mosaic solar loan if the installer lied?

You must prove the misrepresentation in writing. File a dispute with Mosaic and a complaint with the CFPB.

Can I stop paying Mosaic if my solar panels don’t work?

Stopping payments is risky for your credit. It is better to pay “under protest” while filing a formal legal dispute.

What is a UCC-1 filing from Mosaic?

It is a legal notice that Mosaic has a claim on your solar equipment. It must be cleared before you can sell your home.

Can I get out of a solar loan if the company went bankrupt?

Yes, potentially under the FTC Holder Rule. This allows you to hold the lender responsible for the installer’s failure.

Conclusion

Homeowners facing Mosaic solar financing problems often struggle to understand their options. The most important thing you can do right now is to stop feeling “stuck” and start building a paper trail.

If your credit, finances, or home sale are being affected, it may be time to seek legal guidance. Keep records of all contracts, payments, and communications related to your Mosaic financing dispute. Most importantly, do not wait too long to act. Early action can help protect your options.

At Solar Cancellation Companies, we help homeowners understand solar financing disputes, cancellation concerns, and possible next steps with practical, consumer-focused guidance. Contact our team today to start your free contract review.