You find a lower mortgage rate and decide to refinance. The process starts smoothly. Your lender reviews the application, your documents look good, and everything seems on track. Then the title company finds a solar lien or fixture filing connected to the property.

At that point, the refinance process may slow down or pause completely. Many homeowners run into this problem without warning. A mortgage refinance with solar lien issues can still move forward successfully. In this guide, we will walk you through how solar financing affects refinancing, why lenders delay approvals, and what steps can help you avoid common problems before closing.

Can You Refinance a Mortgage With a Solar Lien?

Yes, you can. However, a solar lien mortgage refinance requires extra steps compared to a standard home loan. The solar company must essentially “step aside” to let your new mortgage take the primary position on your home’s title.

How Solar Financing Affects Mortgage Refinancing

When you finance solar panels, the lender often files a UCC-1 statement. This isn’t necessarily a lien on your house, but a lien on the solar equipment itself. Even so, it appears on your title report. Your mortgage lender sees this as a competing claim. They won’t fund your loan until they are sure they are first in line for payment if the house is ever sold.

Why Some Mortgage Lenders Delay or Deny Approval

Lenders hate risk. If they see solar panel lien refinancing issues, they worry about who owns the equipment and who gets paid first. If a solar loan is classified as a PACE lien, many traditional lenders (like those for Fannie Mae or Freddie Mac loans) will deny the application immediately unless the lien is paid off in full.

When Refinancing Is Still Possible

Refinancing is possible when the solar company agrees to a “subordination.” This means they legally agree to stay in a secondary position behind your new mortgage. If you have a standard solar loan and a cooperative lender, the process is usually just a matter of paperwork.

The Difference Between Solar Loans, Leases, and PACE Liens

- Solar Loans: You own the panels. The lender has a lien on the equipment.

- Solar Leases: You don’t own the panels. The solar company owns them and files a fixture filing to protect their assets.

- PACE Liens: These are attached to your property taxes. These are the hardest to manage during a refinance.

Why Solar Liens Cause Problems During Mortgage Refinancing

The primary issue is “priority.” In the world of real estate, the order of who gets paid matters.

Mortgage Lenders Require First Lien Position

Your bank wants to be the “First Lien Holder.” This ensures that if the home is foreclosed, they are the first ones to get the money. A solar lien can sometimes “cloud” this title, making it unclear who has the first right to the property.

How Solar Liens Impact Underwriting

During the mortgage refinance solar contract review, an underwriter will look at your monthly solar payment. They must decide if the solar financing is a personal loan or a real estate lien. This determines how they calculate your debt and your home’s equity.

Debt-to-Income Ratio Issues With Solar Loans

A solar loan affecting mortgage approval often comes down to your Debt-to-Income (DTI) ratio. If your solar payment is high, it might push your DTI over the lender’s limit (usually 43% to 45%). This is a common reason why a refinance is denied because of solar loan obligations.

Why Title Companies Flag Solar Financing

The title company’s job is to ensure the home is “clear.” When they see a UCC-1 filing, they flag it. They won’t issue title insurance to your new lender until the solar company signs a document acknowledging the new mortgage.

Common Reasons Refinancing Gets Delayed

- The solar company takes weeks to respond to a subordination request.

- The lender and the solar company can’t agree on the legal language.

- The homeowner didn’t realize there was a lien until the last week of closing.

Types of Solar Financing That Affect Refinancing Approval

| Financing Type | Impact on Refinance | Difficulty Level |

| Traditional Solar Loan | Requires subordination; usually approved. | Moderate |

| Solar Lease | Requires a “Notice of Independent Ownership.” | Low to Moderate |

| PACE / HERO Loan | Usually must be paid off in full to refinance. | High |

| PPA (Power Purchase Agreement) | Similar to a lease; needs company cooperation. | Moderate |

UCC-1 Fixture Filings Explained

A UCC-1 is a public notice that a lender has an interest in personal property (your panels) attached to real property (your house). While it isn’t a lien on the land, it acts as a “speed bump” for your title. You must address how to refinance a mortgage with an active solar lien by managing this filing.

Which Solar Financing Creates the Biggest Refinance Challenges

PACE financing and property tax liens are the most difficult. Because PACE loans are paid through property taxes, they often take “super-priority” over a mortgage. Most mortgage lenders will refuse to refinance unless the PACE lien is paid off or significantly modified.

What Is Solar Lien Subordination?

Subordination is the “magic word” for refinancing home with solar loan hurdles. It is a legal agreement where one lien holder agrees to stay in a lower priority than another.

How Lien Priority Works During Refinancing

Usually, the oldest lien is the most important. If you got your mortgage in 2020 and solar in 2022, the mortgage is first. But when you refinance in 2026, that new mortgage is “younger” than the 2022 solar lien. Subordination forces the 2022 solar lien to stay “second” in line.

Why Mortgage Lenders Require Subordination

Without it, the solar company could technically claim they have a higher right to the property value than the bank. No bank will take that risk.

How Long Solar Lien Subordination Takes

This is a major source of refinance delays. It typically takes 15 to 30 days. If the solar company is slow, your rate lock expiration risks go up significantly.

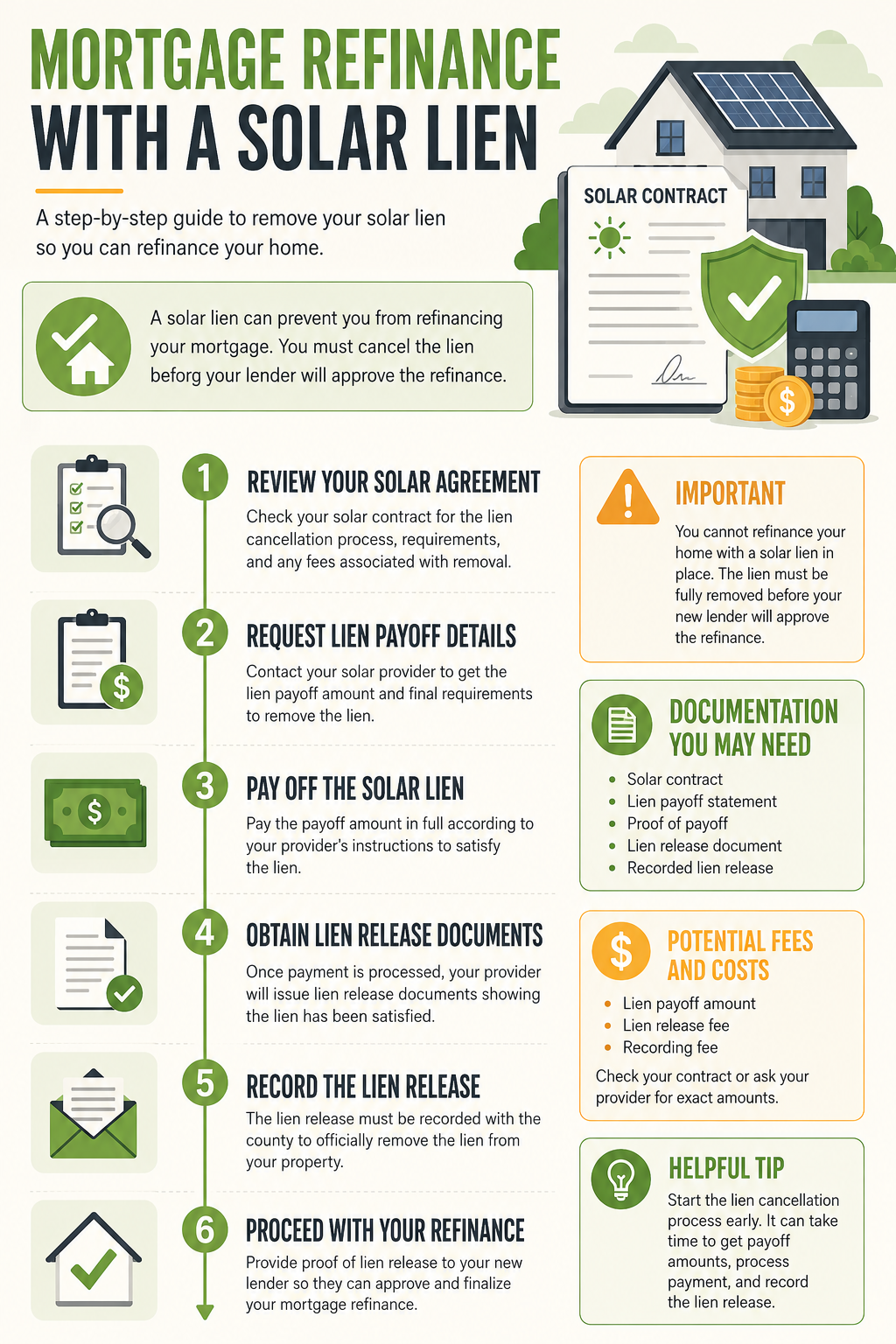

Step-by-Step Process to Refinance a Home With a Solar Lien

If you want to know how to refinance with solar panels financed, follow these steps to get solar lien subordinated during mortgage refinance:

- Identify Your Solar Financing Type: Look at your original contract. Is it a loan, a lease, or PACE?

- Gather Solar Loan and Lien Documents: Have your UCC-1 filing number and your account statement ready.

- Contact Your Solar Financing Company Early: Don’t wait for the lender to do this. Call the “Subordination Department” immediately.

- Request Lien Subordination: Ask specifically for their subordination package. They will likely charge a fee ($100–$300).

- Work With Your Mortgage Lender and Title Company: Give them the contact person at the solar company.

- Complete Underwriting Requirements: Provide proof that the solar payments are current.

- Finalize Closing Without Delays: Follow up every three days until the title company confirms they have the signed subordination form.

Documents Lenders Require for Refinancing With Solar Panels

To avoid missing solar documents causing a crisis, have these ready:

- Original Solar Purchase or Lease Agreement.

- Most recent solar monthly statement.

- The filed UCC-1 Financing Statement (from your county records).

- The solar company’s Subordination Requirements sheet.

Why Mortgage Refinancing Gets Delayed With Solar Financing

Solar Company Bankruptcy or Servicer Changes

If your solar installer went out of business, finding who holds the lien is a nightmare. This is one of the top solar company bankruptcy complications. You may have to track down a third-party servicer to get the lien released or subordinated.

Title Review Problems

Sometimes a title search finds an old lien from a solar company that was already paid off but never “discharged.” This requires a “Release of Lien,” which can take weeks to process through the county.

PACE Liens Blocking Mortgage Approval

If you have a PACE lien, the lender might require you to do a payoff at closing. This means your new mortgage must be large enough to pay off both your old house loan and the entire solar balance.

What Happens if Your Refinance Is Denied Because of a Solar Loan?

If you are refinance denied because of solar loan issues, you have three options:

- Pay off the solar loan: Use cash or part of your equity to eliminate the lien.

- Switch Lenders: Some portfolio lenders are more flexible with solar than big banks.

- Request a Re-Review: If the denial was due to DTI, see if you can count the “utility savings” from the panels as income (though this is rare).

Does a Solar Loan Affect Home Value During Refinancing?

It depends on the appraiser. If you own the panels (loan), they may add value to the home. If you lease them, the appraiser usually gives them zero value because you don’t own the asset.

State-Specific Solar Refinance Issues Homeowners Should Know

Solar Lien Refinance Rules in California

California has the highest number of PACE/HERO loans. Many homeowners here face refinance homes with solar lien near me issues because of how these are taxed. Ensure your lender is familiar with California’s specific solar disclosure laws.

Mortgage Refinance Solar Loan Issues in Texas

In Texas, homestead laws are strict. A mortgage refinance solar loan Texas can be tricky if the solar company didn’t follow specific filing rules. Always check if the UCC-1 was filed correctly at the state level.

Florida Solar Financing and Refinance Delays

Florida’s frequent storms mean many solar companies change hands or go out of business. This creates solar financing refinance Florida delays when trying to find a representative to sign off on subordination.

Frequently Asked Questions

-

Will my solar loan count toward my debt-to-income ratio?

Yes. Lenders treat the monthly solar payment just like a car loan or credit card debt.

-

What is a UCC-1 filing?

It is a “Fixture Filing” that notifies the public that the solar panels are collateral for a loan, even if they are attached to your house.

-

Does the solar company have to agree to subordination?

Technically, no. However, most modern solar lenders have a standard process because they want you to keep your home.

-

What if my solar company is out of business?

You must contact the company that bought their “debt portfolio.” Look at your billing statement to see who you actually pay every month.

-

Can I refinance a PACE lien?

Most lenders require PACE liens to be paid off entirely during the refinance because they hold “super-priority” over the mortgage.

-

How can I speed up the solar subordination process?

Call the solar company daily and offer to pay for “expedited” processing if they offer it.

Final Thoughts on Mortgage Refinancing With Solar Liens

Navigating a mortgage refinance with solar lien doesn’t have to be a deal-breaker. The key is to stop treating the solar panels as a “utility” and start treating them as a “lien” from day one of your application.

If you have a standard solar loan, best ways to refinance a home with financed solar panels involve early communication. Call your solar provider the moment you decide to refinance. Do not wait for your lender to find the lien.

If you have a PACE lien or a lease, be prepared for a more complex “payoff” or “transfer” process. By being proactive and gathering your documents early, you can protect your rate lock and ensure your refinance closes on time. You’ve worked hard for your home equity and don’t let a simple fixture filing stand in the way of a better financial future.