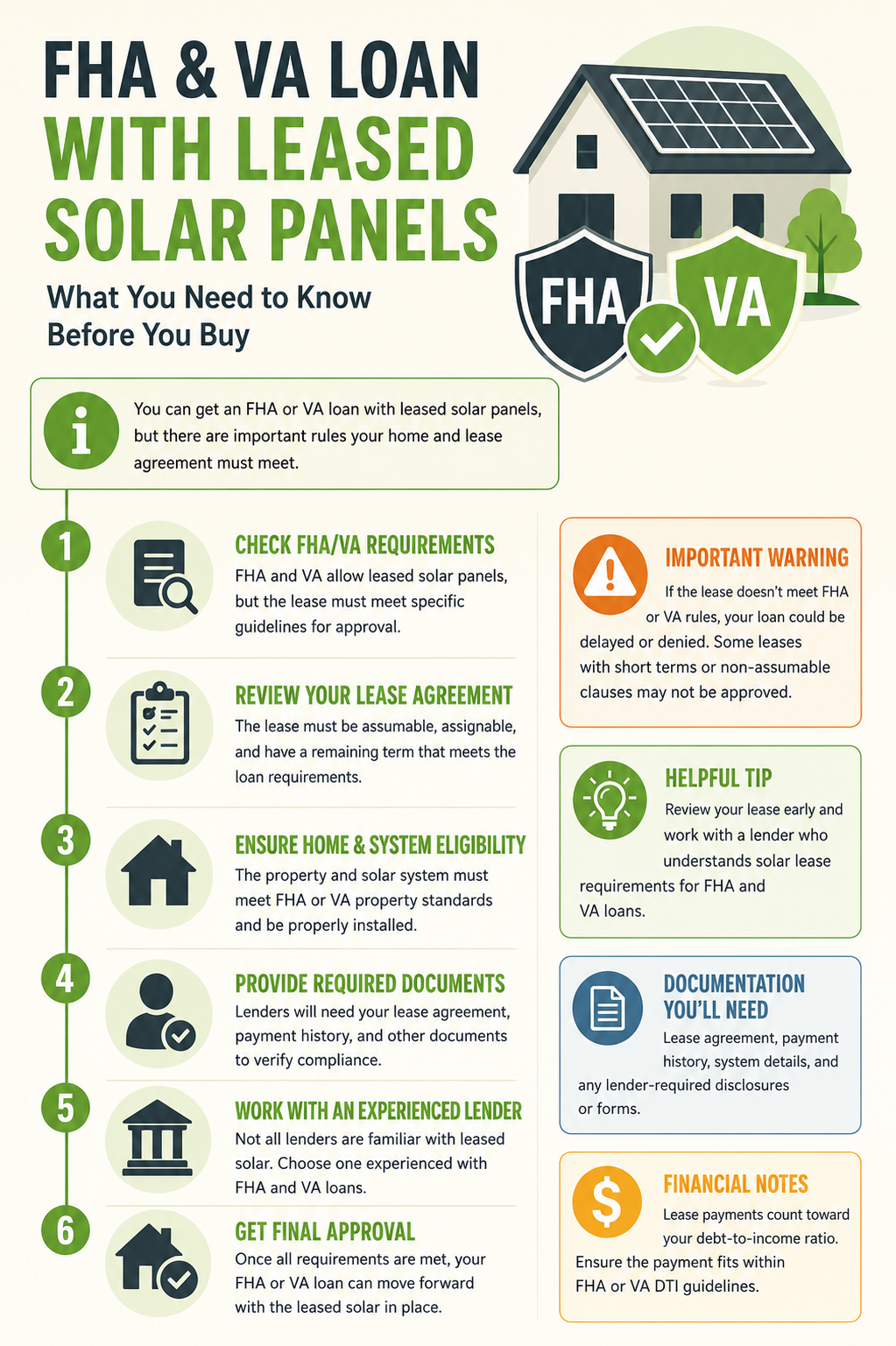

Buying or refinancing a home with leased solar panels can feel simple. But it often catches buyers off guard. The FHA and VA loan with leased solar panels process works differently from a normal home purchase.

The key difference? The solar panels are not owned by the homeowner. A solar company owns them. That one fact changes how lenders, appraisers, and title companies look at the deal.

The good news is that approval is possible. Many buyers close loans on homes with active solar leases every year. What matters most is knowing what lenders check and getting the right papers ready before you apply.

This guide walks you through the whole process. You will learn what FHA and VA lenders look for, what documents to gather, what can slow things down, and what to do if a lender pushes back.

Can You Get Approved for an FHA or VA Loan With Leased Solar Panels?

Yes, you can. But the terms of your solar lease play a big role in how lenders treat the deal.

FHA Loan Approval With Leased Solar Panels

The leased solar panels FHA loan requirements focus on two things: your monthly payment and whether the lease can be passed to a new buyer.

FHA lenders follow HUD rules when they look at these agreements. Since the solar company owns the panels, not the homeowner, the way the home is valued can be affected.

FHA lenders will check:

- Whether the monthly lease payment is counted in your debt load

- Whether the lease can be passed on to a new buyer

- Whether the solar agreement creates any issue with the title

- Whether the panels are fixed to the roof in a way that changes how the home is valued

VA Loan Approval With Leased Solar Panels

VA loan leased solar panels approval works in a similar way. But VA rules give lenders a bit more room to decide. The VA does not ban loans on homes with solar leases.

That said, each lender can set their own rules. Some are stricter than VA minimum standards. Always ask your lender directly what they need.

VA lenders will check:

- That the solar company holds the panels as their own property, not as part of the home

- That the lease does not place a claim on the title

- That the buyer can cover all housing costs, including any lease payments

Situations That May Create Approval Problems

Some solar leases cause more trouble than others. Watch out for these:

- Leases with no transfer clause or very strict transfer terms

- Monthly payments that push your debt ratio too high

- UCC filings that show up on a title search

- Leases with large buyout amounts

- Missing papers from the solar company

How Leased Solar Panels Affect Mortgage Underwriting

Review of Your Monthly Costs

Lenders look at every monthly bill you owe. If your solar lease is $100 a month, some lenders add that to your debt total. This can lower how much home you qualify to buy.

If the buyer takes over the lease, the payment moves with it. Lenders want to know the exact amount due each month and how many months are left on the lease.

Review of What the Home Is Worth

The panels sit on the roof, but the solar company owns them. This creates a question for the home appraiser: do the panels add value?

Most appraisers do not add value for leased panels since the buyer does not own them. The home is still valued, but lenders want written proof of who owns the equipment.

Review of the Title and Legal Records

Part of understanding how leased solar panels affect home loan underwriting decisions is knowing how the title search works. Solar companies often file a legal document called a UCC-1 to protect the gear they own.

This filing can show up on a title report and look like a lien. Lenders and title companies will flag it. It does not kill the deal, but it has to be sorted out before you can close. If you are also dealing with a mortgage refinance with a solar lien, the same UCC filing process applies and requires the same early attention.

Documents Needed for FHA and VA Loan Review

Pulling together the right documents needed for mortgage approval with leased solar systems early saves time. Here is what most lenders ask for:

- Full solar lease agreement including all updates and add-ons

- Monthly payment amount for now and future periods

- Payment history showing all payments are up to date

- Transfer clause details showing how the lease can be passed to a new buyer

- Buyout figure if the buyer or seller wants to pay off the lease early

- UCC filing info for any legal filings the solar company has on record

- Solar company contact info so the lender or title company can reach them

- Proof of lease ownership confirming the panels are leased, not owned by the homeowner

- Lender forms since some lenders have their own solar check sheets

Common Issues That Can Delay Loan Approval

Missing or Incomplete Solar Papers

Incomplete paperwork is the top cause of solar lease mortgage issues that slow down a closing. If the lender cannot confirm the lease terms, they cannot approve the loan.

Solar companies can be slow to reply. Contact them as soon as the home goes under contract. Do not wait until last week.

Leases That Cannot Be Passed to a New Buyer

Some older leases have no transfer option. Others require the buyer to pass a credit check before taking over. If the lease cannot be passed on, the seller may need to pay it off before closing.

Payment or Contract Problems

Missed solar payments or open disputes with the solar company can cause delays. Lenders need proof that the contract is in good standing. Fix any payment issues before you apply.

High Monthly Costs That Affect Qualification

This is one of the most common ways solar lease affecting mortgage approval plays out. If the solar payment pushes the combined housing cost too high, the lender may cut the loan amount or say no.

Check your numbers before you apply. Know your total monthly payment including the lease, and ask your lender how they count it.

Title Concerns

UCC filings and other solar entries on the title report must be checked by the title company. This takes time. Getting the title search done early gives you room to fix any issues.

UCC Filings and Solar Liens Explained

What Is a UCC Filing?

A UCC-1 financing statement is a legal form. A company files it to say they own certain property, even if that property is at someone else’s address. Solar companies file these to protect the panels they own but install at your home.

How UCC Filings Differ From Property Liens

A property lien is tied to the home itself. A UCC filing is tied to a piece of equipment. The solar panels are the solar company’s property, not part of the real estate. So the UCC filing is not a lien on your home.

Still, it can look like one on a title report. That is why title companies flag it for review.

Why Lenders Review Them

Lenders want to be sure the solar company has no claim on the home itself, only on the equipment. If the filing is set up the right way, it should not block the mortgage.

Can These Issues Delay Closing or Refinancing?

Yes. If the UCC filing is unclear or set up wrong, the title company may need to contact the solar firm for a fix or a side agreement. This can add days or even weeks to the process. Plan ahead.

Buying a Home Versus Refinancing a Home With Leased Solar Panels

The steps involved when you refinance with leased solar panels are close to buying, but not the same. Here is a side by side look:

| Factor | Buying a Home | Refinancing a Home |

| Solar lease transfer | Buyer must qualify to take over the lease | Owner keeps the current lease |

| DTI impact | Lease payment added to buyer’s debt total | Lease payment already in place |

| Documents needed | Seller must supply full lease details | Owner provides their own papers |

| Title review | New title search is required | Title is checked again for the new loan |

| Appraisal treatment | Panels add no value since they are leased | Panels add no value since they are leased |

| Key risk | Transfer is denied or delayed | UCC filings or high debt ratio block approval |

| Timeline impact | Slow solar company can push back closing date | Title issues can add weeks to the process |

How Solar Lease Transfers Work During Home Sales

Knowing how to transfer a solar lease when buying or selling a home is key to a smooth closing.

Steps to Transfer a Solar Lease

- The seller tells the solar company the home is being sold

- The solar company sends a transfer form to the buyer

- The buyer fills out the form and shares their financial info

- The solar company checks the buyer’s credit and gives a yes or no

- A new lease is signed in the buyer’s name

- The transfer is confirmed and sent to the lender

What Happens if a Lender Rejects a Property With Leased Solar Panels?

Knowing what happens if a lender rejects a property with leased solar panels helps you stay calm and think clearly.

A rejection does not always mean the deal is over. Here is what usually comes next:

- More document requests. The lender may ask for extra papers from the solar firm, the seller, or the title company before they make a final call.

- Other loan options. Some lenders know solar leases well. If your current lender says no, try shopping for one with more experience in this area.

- Price talks. Buyers can ask the seller to lower the price if the solar lease is making the loan harder to get.

- Lease change or buyout. The seller or buyer can work with the solar firm to change the lease terms or pay it off. That clears the way for approval.

Frequently Asked Questions

Can you get approved for an FHA loan with leased solar panels?

Yes. FHA loans can be approved when the lease can be passed on, the payments fit within your debt limits, and the title is clear. You just need to give the lender the right documents.

What do lenders need for VA loan approval with solar lease agreements?

VA lenders usually want the full lease agreement, proof it can be transferred, written proof the panels are leased and not owned, and a clean title with any UCC filings noted properly.

Can a solar lease delay FHA or VA home loan approval?

Yes. Missing papers, slow solar company replies, or open UCC filing issues are the main causes of delay. Starting the paperwork process early is the best way to avoid this.

Does a solar lease count toward the debt-to-income ratio?

It depends on the lender. Some count the monthly payment as part of your debt. Others do not, if the lease is passed on to the buyer. Ask your lender directly before you apply.

Can leased solar panels affect refinancing approval?

Yes. The same review process applies when you refinance. Lenders will look at the lease terms, your monthly costs, and the title to make sure nothing blocks the new loan.

How to Move Forward With Confidence

Leased solar panels do not have to stop your home purchase or refinance. But they do require more prep, faster action, and better planning than a normal deal.

The more ready you are before the underwriting review, the smoother your closing will be. If your solar agreement is creating delays or uncertainty during a home purchase or refinance, contact SCC today to explore your options and get guidance on the next steps before small issues become bigger obstacles.